It’s been a while since we have reviewed finance conditions, and I think it is worth reviewing this all important condition again. The ‘standard’ finance condition isn’t too bad – as long as you understand what the condition requires and when it won’t suit your needs as a purchaser.

In this article, we will cover the requirements of the standard finance condition and its limitations. However, take care that your proposed contract does in fact include the standard condition, as there is an increasing trend towards non-standard finance conditions.

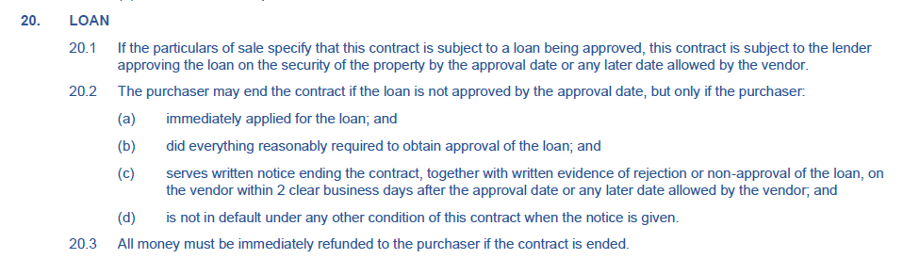

The Standard Condition

The Standard finance condition in the current LIV / REIV contract is as follows:

Points to Note

There are a number of key points for purchasers to note:

- The clause will usually only apply if you have inserted the details of your lender, loan amount and deadline for approval in the Particulars of Sale;

- The contract doesn’t automatically end if your finance is declined or approval is delayed. If there is a problem, you need to advise the vendor that the contract is terminated or that you need an extension of time;

- Your right to terminate the contract under the finance condition is in turn conditional on your having made immediate application for the loan, having done what is required to get approval and not otherwise being in default (eg payment of deposit).

When the Finance Condition Doesn’t Work

There are a couple of common situations where this finance condition isn’t appropriate.

The first involves situations where you intend to build a home – whether that be as a house and land package or otherwise. If the land purchase price is $500,000 and subject to a finance condition for $400,000 – you might find that the vendor won’t allow you to terminate the contract if you apply for a $750,000 loan to cover your building costs as well.

If you are in this situation, it would be advisable to tailor the finance condition – and also make your purchase contract conditional upon an acceptable building contract being signed.

Another situation where the finance condition doesn’t work is where the purchaser is looking to raise funds from investors to settle the purchase. If the Purchaser is unsuccessful in obtaining investor funds, the vendor may refuse the allow the contract to be terminated under the standard finance condition. Again, a tailored special condition would be more appropriate.

The Most Ridiculous Thing

In the course of obtaining finance against an investment property owned by my family trust, the lender enquired (amongst numerous other requests) as to the proposed use of the funds. I said that I was renovating my principal place of residence – because that was the truth.

This led to an enquiry as to where I would be living during the renovation. How exactly this was relevant to a financier lending money against a property owned by my trust is beyond me.

Interestingly, it also led to a discussion with some mortgage brokers who pointed out that when obtaining finance for renovations it was better to say that they were minor or cosmetic renovations – not major renovations. Given the need for building permits and builders warranty insurance for even relatively minor renovations – I really don’t understand this either!

Lewis O’Brien & Associates

As always, we continue to offer phone / zoom purchase contract reviews for $165.00 (inc GST). In an environment where standard conditions are less and less standard and property prices continue to rise I strongly recommend this service before you sign a contract.

You can book a session with me here

Next Time

In the next newsletter I want to explore stamp duty in the context or raising funds for property development. This is a complex area that it is important to get right.

Lewis O’Brien

Your Preferred Property Lawyer